Before you start looking for your dream home, it’s essential to understand your financial health. This involves evaluating your income, expenses, debts, and savings to determine how much you can afford to spend on a home.

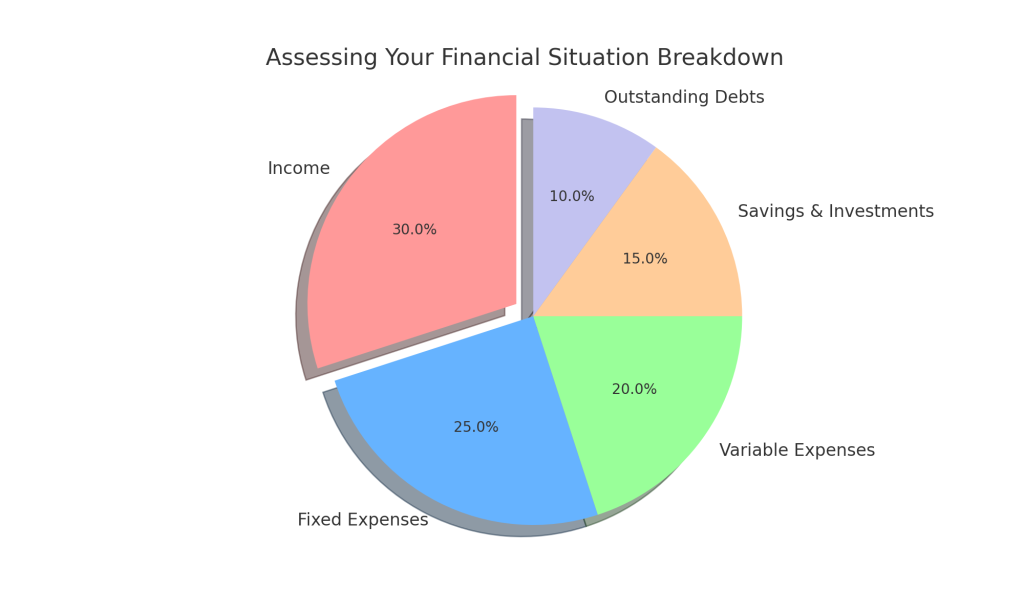

Financial Situation Breakdown: This pie chart provides a visual representation of the key components you should consider when assessing your financial situation:

- Income (30%): Total monthly income, including salaries, wages, bonuses, and other sources.

- This represents your total monthly income, including all consistent sources such as salaries, wages, bonuses, freelance work, rental income, and investments. Accurately assessing your income is the first step to understanding how much you can allocate towards a new home.

Fixed Expenses (25%): Regular monthly expenses such as rent, utilities, car payments, insurance, and loans.

- Fixed expenses are regular, predictable monthly costs such as rent, utilities, car payments, insurance, and loans. These expenses remain relatively stable each month and are essential to consider when setting your home buying budget.

Variable Expenses (20%): Discretionary spending like groceries, entertainment, and dining out.

- Variable expenses include discretionary spending that can fluctuate from month to month, such as groceries, entertainment, dining out, and other personal expenditures. Tracking these can help you identify areas where you can save more.

Savings & Investments (15%): Contributions to savings accounts, retirement funds, and other investments.

- Regular contributions to savings accounts, retirement funds, and other investments are crucial for long-term financial health. Ensure you have an emergency fund and start saving for your down payment and closing costs.

Outstanding Debts (10%): Total outstanding debts including credit cards, student loans, car loans, and personal loans.

- This includes all current debts such as credit cards, student loans, car loans, and personal loans. Understanding your debt-to-income ratio is essential for securing a mortgage and managing your finances responsibly.

By thoroughly assessing your financial situation, you’ll have a clear understanding of what you can afford and be better prepared to navigate the home buying process. This careful preparation will help you set a realistic budget and avoid financial stress, making your journey to homeownership smoother and more enjoyable.